| Pages in topic: [1 2] > | VAT - dealing with client outside EU Thread poster: Usa Sukdapisumpun

|

|---|

I am new in Proz and would like to ask some advise.

I am a freelance translator living in the Netherlands. I have a question about VAT with customers from outside the EU. I have checked with my tax authorities, but that is not entirely clear. The website say that ....as a translator in the Netherlands and my client is outside EU, I have to ask the tax authority in the country where my customer live about how to file VAT.... How you all do it? How to contact them?, They do not all talk En... See more I am new in Proz and would like to ask some advise.

I am a freelance translator living in the Netherlands. I have a question about VAT with customers from outside the EU. I have checked with my tax authorities, but that is not entirely clear. The website say that ....as a translator in the Netherlands and my client is outside EU, I have to ask the tax authority in the country where my customer live about how to file VAT.... How you all do it? How to contact them?, They do not all talk English. It isn’t a customer’s task who should find out about VAT and provide me the information ? ▲ Collapse

| | | | RobinB

United States

Local time: 09:04

German to English

| Not at all relevant | Jul 19, 2020 |

Hi Usa,

VAT is a non-issue for clients outside the EU ("third-country" clients in EU-speak).

You do not charge VAT on your invoice, and any VAT, GST, sales or similar tax due on the service in your client's home country is a matter for the client, not you. You don't have to contact any tax authorities in any third countries.

So invoicing clients outside the EU is actually about as simple as you can get!

| | | |

RobinB wrote:

Hi Usa,

VAT is a non-issue for clients outside the EU ("third-country" clients in EU-speak).

You do not charge VAT on your invoice, and any VAT, GST, sales or similar tax due on the service in your client's home country is a matter for the client, not you. You don't have to contact any tax authorities in any third countries.

To be precise, you mean 'outside the EU’s VAT area (and the UK until the end of the Brexit transition period)', which is not exactly the same as the EU.

See https://ec.europa.eu/taxation_customs/business/vat/eu-vat-rules-topic/territorial-status-eu-countries-certain-territories_en for a complete list.

As far as I'm aware, the EU itself is the only region in the world that requires third-country sellers of services to EU residents to charge EU VAT, so I guess the local tax authorities think everybody does like the EU.

| | | | Sheila Wilson

Spain

Local time: 15:04

Member (2007)

English

+ ...

| EU VAT area isn't exactly the EU area | Jul 19, 2020 |

Thomas T. Frost wrote:

To be precise, you mean 'outside the EU’s VAT area (and the UK until the end of the Brexit transition period)', which is not exactly the same as the EU.

I live in the Canary Islands -- I'm in Spain, in the EU, and in the euro zone. But if you're in the EU and you order work from me, I won't add VAT. The Canary Islands are outside its scope.

| | |

|

|

|

Samuel Murray

Netherlands

Local time: 16:04

Member (2006)

English to Afrikaans

+ ...

Usa Sukdapisumpun wrote:

I have checked with my tax authorities, but that is not entirely clear. The website say that ... as a translator in the Netherlands and my client is outside EU, I have to ask the tax authority in the country where my customer live about how to file VAT.

Here's how it works (for services):

1. If your client is in the Netherlands, you should add VAT on the invoice at the Dutch VAT rate. If your client has a VAT number, write it on the invoice. Declare this income in your quarterly VAT returns.

2. If your client is in the EU (not the Netherlands) and has a VAT number, you should write "VAT shifted" (or "BTW verlegd") on the invoice and not add any VAT. Write your client's VAT number on the invoice. Declare this income in your quarterly VAT returns. Also remember to fill in an ICP VAT form.

3. If your client is in the EU and does not have a VAT number, you should add VAT on the invoice at the Dutch VAT rate. Declare this income in your quarterly VAT returns.

4. If your client is not in the EU and is a business, you should not add VAT on the invoice. Do *not* declare this income in your quarterly VAT returns.

5. If your client is not in the EU and is not a business, you should add VAT on the invoice at the Dutch VAT rate. Declare this income in your quarterly VAT returns.

It is true that in case of point #4 above, you have to find out if the client's country requires you to file any tax returns in their country, but I don't know of any instance where that is actually so. The Dutch tax authorities consider the service to have been rendered in your client's country, so theoretically speaking it's up to you to make sure that you are not required to pay taxes in that country.

[Edited at 2020-07-19 20:44 GMT]

| | | | | #5 is in conflict with EU law | Jul 19, 2020 |

Samuel Murray wrote:

5. If your client is not in the EU and is not a business, you should add VAT on the invoice at the Dutch VAT rate. Declare this income in your quarterly VAT returns.

The Dutch tax authorities consider the service to have been rendered in your client's country

We have talked about this before. According to EU law (the VAT Directive), no VAT is due for any type of client outside the EU's VAT area. As you say, the place of supply is outside the EU, so no VAT is due. VAT is a tax on consumers in the EU, not on consumers in the rest of the world.

| | | | Samuel Murray

Netherlands

Local time: 16:04

Member (2006)

English to Afrikaans

+ ...

| Not too happy about the misquote | Jul 20, 2020 |

Thomas T. Frost wrote: Samuel Murray wrote:

5. If your client is not in the EU and is not a business, you should add VAT on the invoice at the Dutch VAT rate. Declare this income in your quarterly VAT returns.

...

The Dutch tax authorities consider the service to have been rendered in your client's country... We have talked about this before. According to EU law (the VAT Directive), no VAT is due for any type of client outside the EU's VAT area. As you say, the place of supply is outside the EU, so no VAT is due. VAT is a tax on consumers in the EU, not on consumers in the rest of the world.

I don't mind that you disagree with me, but this is a misquote. My intention was clearly that the sentence "the Dutch tax authorities consider the service to have been rendered in your client's country" relate to #4, not #5.

Anyway, the OP is from the Netherlands. Usa, what Thomas and I are disagreeing here is the "place of supply", which is a legal term which relates to an assumption of tax jurisdiction. A service may be physically rendered in one place while it's "place of supply" may be somewhere else. (Also, when you google for this yourself, or fill in your VAT returns, note that there are different rules for goods and for services, and although [most?] translators consider their work to be "goods" for copyright purposes, for tax purposes it is a service.)

I hope Thomas will supply a URL of his own, but in the mean time, my googling got me this page:

https://ec.europa.eu/taxation_customs/business/vat/eu-vat-rules-topic/where-tax_en#supply_services

which I can't vouch for, but which agrees with my point of view.

| | | | | Not a misquote | Jul 20, 2020 |

Samuel Murray wrote: Thomas T. Frost wrote: Samuel Murray wrote:

5. If your client is not in the EU and is not a business, you should add VAT on the invoice at the Dutch VAT rate. Declare this income in your quarterly VAT returns.

...

The Dutch tax authorities consider the service to have been rendered in your client's country... We have talked about this before. According to EU law (the VAT Directive), no VAT is due for any type of client outside the EU's VAT area. As you say, the place of supply is outside the EU, so no VAT is due. VAT is a tax on consumers in the EU, not on consumers in the rest of the world. I don't mind that you disagree with me, but this is a misquote. My intention was clearly that the sentence "the Dutch tax authorities consider the service to have been rendered in your client's country" relate to #4, not #5.

I quoted what you wrote. If you wrote something else than what you meant, it's clearly not my fault.

So what did you intend to write under #5?

Samuel Murray wrote: Anyway, the OP is from the Netherlands. Usa, what Thomas and I are disagreeing here is the "place of supply", which is a legal term which relates to an assumption of tax jurisdiction. A service may be physically rendered in one place while it's "place of supply" may be somewhere else. (Also, when you google for this yourself, or fill in your VAT returns, note that there are different rules for goods and for services, and although [most?] translators consider their work to be "goods" for copyright purposes, for tax purposes it is a service.) I hope Thomas will supply a URL of his own, but in the mean time, my googling got me this page: https://ec.europa.eu/taxation_customs/business/vat/eu-vat-rules-topic/where-tax_en#supply_services which I can't vouch for, but which agrees with my point of view.

[/quote]

https://ec.europa.eu/taxation_customs/business/vat/eu-vat-rules-topic/where-tax_en#supply_services :

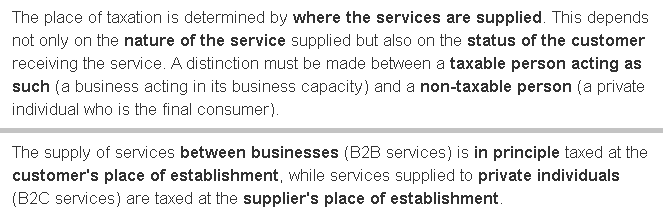

'B2C services like advertising services, services of consultants and lawyers, financial services,telecommunications services, broadcasting services and electronically supplied services are taxed at the place where the customer is established provided the customer is established in a non-EU country [Article 59 of the VAT Directive].

Example 47: When a Hungarian company sells an anti-virus programme to be downloaded through its website to private individuals residing in Australia, there will be no VAT due in Hungary.

Example 48: Services rendered by a Belgian lawyer to a US professor will not be subject to VAT in Belgium.'

There you have it from the horse's mouth. You should not add VAT to any services, whether B2B or B2C, if the client is not located in the EU's VAT area.

As for translations being 'goods' for copyright purposes, I have no idea what you are referring to. Copyright relates to intellectual property, which is immaterial.

| | |

|

|

|

Samuel Murray

Netherlands

Local time: 16:04

Member (2006)

English to Afrikaans

+ ...

Thomas T. Frost wrote:

B2C services like advertising services, services of consultants and lawyers, financial services,telecommunications services, broadcasting services and electronically supplied services...

If your accountant had told you that translation services are also meant by this exception, then of course we can say no more.

This may be something for Usa to ask her accountant: does he/she believe that translation services are sufficiently "like" advertising services, services of consultants and lawyers, financial services, telecommunications services, broadcasting services and electronically supplied services to be covered by this exception. My impression is "no": this exception does not mean translation services.

[Edited at 2020-07-20 13:40 GMT]

| | | | | The EU's impression is 'yes' | Jul 20, 2020 |

Samuel Murray wrote: Thomas T. Frost wrote:

B2C services like advertising services, services of consultants and lawyers, financial services,telecommunications services, broadcasting services and electronically supplied services... If your accountant had told you that translation services are also meant by this exception, then of course we can say no more. This may be something for Usa to ask her accountant: does he/she believe that translation services are sufficiently "like" advertising services, services of consultants and lawyers, financial services, telecommunications services, broadcasting services and electronically supplied services to be covered by this exception. My impression is "no": this exception does not mean translation services.

See https://ec.europa.eu/taxation_customs/sites/taxation/files/guidelines-vat-committee-meetings_en.pdf :

4. QUESTIONS CONCERNING THE APPLICATION OF COMMUNITY VAT PROVISIONS

4.2 Origin: Portugal

References: Article 9 of the Sixth VAT Directive

Subject: Place of taxation of translators’ and interpreters’ services

(Document TAXUD/1873/00 – Working Paper No 302)

All delegations agree that translation services are among the services covered by Article 9(2)(e).

The great majority of delegations agree that interpretation services are also among the services covered by Article 9(2)(e).

Article 9(2)(e):

https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX:31977L0388

Article 9

Supply of services

1. The place where a service is supplied shall be deemed to be the place where the supplier has established his business or has a fixed establishment from which the service is supplied or, in the absence of such a place of business or fixed establishment, the place where he has his permanent address or usually resides.

2. However: […]

(e) the place where the following services are supplied when performed for customers established outside the Community or for taxable persons established in the Community but not in the same country as the supplier, shall be the place where the customer has established his business or has a fixed establishment to which the service is supplied or, in the absence of such a place, the place where he has his permanent address or usually resides: - transfers and assignments of copyrights, patents, licences, trade marks and similar rights,

- advertising services,

- services of consultants, engineers, consultancy bureaux, lawyers, accountants and other similar services, as well as data processing and the supplying of information,

- obligations to refrain from pursuing or exercising, in whole or in part, a business activity or a right referred to in this point (e),

- banking, financial and insurance transactions including reinsurance, with the exception of the hire of safes,

- the supply of staff,

- the services of agents who act in the name and for the account of another, when they procure for their principal the services referred to in this point (e).

My former German accountant is of the same opinion.

It also makes sense. The EU requires that EU VAT be paid for services supplied to EU residents by third countries. I.e. services must be taxed in the customer's country of residence. It would be incoherent also to require that EU VAT be paid for services supplied to non-EU residents.

| | | | RobinB

United States

Local time: 09:04

German to English

| Certain services only... | Jul 20, 2020 |

Thomas T. Frost wrote: As far as I'm aware, the EU itself is the only region in the world that requires third-country sellers of services to EU residents to charge EU VAT, so I guess the local tax authorities think everybody does like the EU.

That applies only to a narrowly defined set of services, and not for example to translations.

| | | | RobinB

United States

Local time: 09:04

German to English

| Thomas, you are correct | Jul 20, 2020 |

Thomas T. Frost wrote: We have talked about this before. According to EU law (the VAT Directive), no VAT is due for any type of client outside the EU's VAT area. As you say, the place of supply is outside the EU, so no VAT is due. VAT is a tax on consumers in the EU, not on consumers in the rest of the world.

No VAT is charged on either B2B or B2C translations where the customer is outside the EU VAT area. But: The suppliers must themselves add (output) VAT on the invoice amount at the relevant rate to their VAT return, and reclaim exactly the same amount as input tax.

| | |

|

|

|

| No declaration | Jul 20, 2020 |

RobinB wrote:

But: The suppliers must themselves add (output) VAT on the invoice amount at the relevant rate to their VAT return, and reclaim exactly the same amount as input tax.

Surely not. When the place of supply outside the EU's VAT area makes such a transaction non-taxable, then there is no VAT of any kind to declare, whether input or output or both. Can you provide any reliable source for this?

The amount of supplies to other member states via the reverse VAT procedure have to be declared, of course, and with a separate list of the VAT numbers of the clients, but no VAT has to be calculated on this amount, as it is not taxable in the translator's own member state.

However, if a VAT-registered translator in the EU's VAT area buys services or products from outside their own member state (via reverse VAT in the case of a supplier in the EU), they must declare input VAT and then deduct the same amount as output VAT.

| | | | Samuel Murray

Netherlands

Local time: 16:04

Member (2006)

English to Afrikaans

+ ...

| @Thomas, you appear to be correct after all | Jul 20, 2020 |

A sweet URL that appears to clinch it.

It would be incoherent also to require that EU VAT be paid for services supplied to non-EU residents.

I would not have considered that illogical at all, since the article in question relates to an *exception*.

RobinB wrote:

The suppliers must themselves add (output) VAT on the invoice amount at the relevant rate to their VAT return, and reclaim exactly the same amount as input tax.

I'm not sure what you mean with "output VAT" and "input tax". (I'm assuming we're talking about translation services here, which does not involve the selling of goods.)

In the Netherlands, the translator only declares VAT on his VAT return if he actually added it to the invoice. The information submitted in the VAT return must correspond with the information on the invoice. Is this what you mean?

However, if a VAT-registered translator in the EU's VAT area buys services or products from outside their own member state (via reverse VAT in the case of a supplier in the EU), they must declare input VAT and then deduct the same amount as output VAT.

Fortunately, I don't ever do that, so I'm always spared the complexities of that particular point. (-:

[Edited at 2020-07-20 17:21 GMT]

| | | | | Coherent or not coherent | Jul 20, 2020 |

Samuel Murray wrote: It would be incoherent also to require that EU VAT be paid for services supplied to non-EU residents. I would not have considered that illogical at all, since the article in question relates to an *exception*.

True, we can debate this. Fortunately it has no bearing on the question of whether to add VAT in such cases.

The VAT Directive and the principle of VAT were invented at a time when cross-border distance selling was a marginal phenomenon and services and goods were something you bought from Mr or Mrs Local around the corner. As reality evolved and the VAT Directive had to keep up with new ways of doing business, layer after layer of exceptions and exceptions to exceptions had to be added, to the extent that the rules today are incredibly complex. Old systems of taxation were never designed for our connected world, but all that is another debate for another day.

So, to conclude:

• National: B2B and B2C client in same member state: VAT.

• EU VAT area: B2C or non-VAT-registered B2B client in other member state: VAT in seller's member state.

• EU VAT area B2B: reverse VAT if B2B client VAT registered and their number passes a VIES check (one should retain evidence of that). Summary of amounts and VAT numbers to be transmitted to national tax authorities.

• Non-EU VAT area: no VAT in any case.

One should pay attention to the territorial exceptions mentioned at https://ec.europa.eu/taxation_customs/business/vat/eu-vat-rules-topic/territorial-status-eu-countries-certain-territories_en , as previously mentioned. For example, Monaco is outside the EU but treated as France for the purpose of VAT.

| | | | | Pages in topic: [1 2] > | To report site rules violations or get help, contact a site moderator: You can also contact site staff by submitting a support request » VAT - dealing with client outside EU | Protemos translation business management system | Create your account in minutes, and start working! 3-month trial for agencies, and free for freelancers!

The system lets you keep client/vendor database, with contacts and rates, manage projects and assign jobs to vendors, issue invoices, track payments, store and manage project files, generate business reports on turnover profit per client/manager etc.

More info » |

| | CafeTran Espresso | You've never met a CAT tool this clever!

Translate faster & easier, using a sophisticated CAT tool built by a translator / developer.

Accept jobs from clients who use Trados, MemoQ, Wordfast & major CAT tools.

Download and start using CafeTran Espresso -- for free

Buy now! » |

|

| | | | X Sign in to your ProZ.com account... | | | | | |